For veterans and active-duty service members, VA (Veterans Affairs) home loans are an attractive option…

10 Interesting Facts About VA Loan Eligibility

Do you know if you’re eligible for a VA home loan? While it’s ultimately up to the Veterans Administration, here are 10 Interesting Facts About VA Loan Eligibility that can help you understand the benefits of getting the single best home loan program in existence!

A VA loan can be an excellent way to buy a home. The government-backed mortgage program has several unique features that save borrowers cash both upfront and every month.

In fact, it’s one of the few programs out there that allows for 100% loan to value (LTV), meaning you could finance the full price of your home. What’s more, private mortgage insurance (PMI) is never allowed – even when you put zero down.

Who wouldn’t love a loan with no down payments and no PMI? Of course, most would, but it is important to remember that borrowers still pay a VA Funding Fee, and the zero-down option depends on the borrower’s entitlement.

These loans aren’t for everybody – VA loan eligibility must be earned. To find out if you’re eligible for a VA loan, get in touch with us now.

-

Eight Uniformed Services Have VA Home Loan Benefits

When most people think of VA loan eligibility, the main military branches come to mind. But did you know there are a total of eight uniformed branches in all that have home loan benefits? Here they are:

- Army

- Navy

- Air Force

- Marines

- Space Force

- Coast Guard

- National Oceanic Atmospheric Administration (NOAA)

- Public Health Service (USPHS)

For commissioned officers of NOAA and the USPHS, you may have access to VA loans. Please check the VA website for full details.

-

VA Loan Eligibility is Earned

Servicemembers are generally told that they will be eligible for a VA loan if they stay in the service long enough. For the most part, service requirements are as follows:

- 2 years for regular service members

- 6 years for Reservists and National Guard members

- 90 days of active duty during wartime

- 181 days of active duty during peacetime

Are You Eligible for VA Home Loan Benefits?

If you’re not sure if you served long enough, don’t worry! You may still be eligible for a VA loan.

-

Reserve/National Guard Members Can Be Eligible Too

Reservists can also earn eligibility for VA home loan benefits. If you’re currently serving in a Reserve Unit or in National Guard, you’re eligible for this great benefit after six years of service.

If you served active duty, you earn your VA home loan benefits faster. During the Iraq War, many Reservists were deployed to active duty. If you were, you could be eligible under active-duty wartime (90 days or period ordered) rules.

Here’s how the Reserve and Guard members typically earn eligibility:

- Six Years of Service, and

- Discharged honorably, or

- Placed on the retired list, or

- Transferred to Standby or Ready Reserve after honorable service, or

- Continue to serve in Selected Reserve

Again, be sure to check the VA website for more information.

-

VA Home Loan Benefits earned through Active Duty

If you’re on active duty or called up for active-duty service, you’re going to earn your VA Home Loan benefits faster than those in the reserves. (Requirements vary for periods.) Here is a summary of active-duty requirements:

- 90 continuous days for active duty service members

- 90 days of active service for current Guard and Reserve servicemembers

- 90 total days for wartime Veterans until 05/07/1975

- 181 continuous days for peacetime Veterans until 09/07/1980 (10/16/1981 for officers)

- At least 181 days or full call for peacetime Veterans 09/08/1980 – 08/01/1990 (10/17/1981 beginning date for officers)

- At least 90 days or full call for Gulf War Veterans 08/02/1990 – Present

It may be hard to keep all the dates straight to determine your own eligibility. If you need help, just get in touch with us and we can help.

-

Surviving Spouses Can Earn Eligibility

Military spouses play a vital role not just in holding down the home front, but also as a support unit to their loved ones who serve. Spouses experience just as much uncertainty, stress, and unfortunately even tragic loss as their Servicemember spouses.

Surviving spouses may also be eligible for VA loans if a husband or wife died while on duty or from a duty-related injury. Additionally, when a Veteran dies of any cause, a spouse may apply for a VA loan if the Veteran lived with a duty-related condition for a period designated by the VA and is eligible for compensation at the time of death.

You may be eligible for a VA loan if you’re a spouse who survived one of the following:

- Veterans who died on duty, or of duty-related causes

- Disabled Veterans eligible for compensation

- POW or MIA

Surviving spouses should check with the VA about all the available bereavement benefits during this difficult time.

-

Other Members Can Earn Eligibility

Veterans of the eight total branches, National Guard/Reservists, and surviving spouses aren’t the only people who are eligible for VA loans. In fact, several other groups may be eligible, including:

- West Point Cadets

- Air Force Academy Cadets

- Coast Guard Academy Cadet

- Naval Academy Midshipmen

- POWs

Of course, certain rules apply. For more details on VA loan eligibility, just fill out our quick online form and one of our representatives will get in touch with you.

-

Those with Abbreviated Service May Still Be Eligible

Things happen, and sometimes those in service are discharged early for a host of reasons. That being said, it is still possible to earn your VA Home Loan benefits if you did not meet the minimum service time requirements. Here are some potential reasons for early discharge where you may still be eligible:

- Hardship

- Government convenience

- Reduction in force

- Certain medical conditions

- Service-connected disability

If you were discharged early for a reason other than dishonorable, it’s worth checking to see if you’re eligible.

-

The Target Property Must Also Be Eligible

You should know that the home you buy has to meet VA minimum property requirements (MPRs), and that only certain kinds of homes can be financed with a VA loan.

What Can You Buy with a VA Loan?

During your application process, a VA-certified appraiser will check to make sure the property meets MPRs. The home must be safe, and sanitary, and have a good foundation, structure, and roof.

The appraiser will also look for basic requirements like clean water, heat, power, and no potential health hazards. Any home with pests, mold, wood rot, or broken windows will not be eligible. The home must also have year-round access on a well-maintained road (private driveways in rural areas are permitted as of January 2023). Other requirements include distinct living areas for sleeping, cooking, dining, and bathing.

All these requirements have been put in place so that Veterans and Servicemembers are protected against buying homes in unlivable conditions.

-

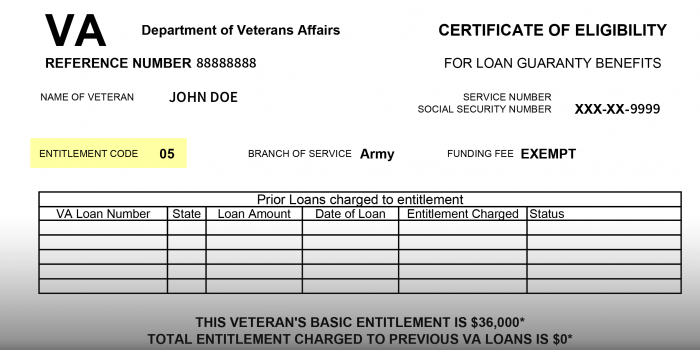

Your Certificate of Eligibility is Required

Any doubts you may have about your entitlement to VA home loan benefits can be put to rest by obtaining a certificate of eligibility (COE). A COE is proof you’re eligible. If you think you may be eligible, get your COE. We’ll need this document before we can consider you for a VA-backed loan.

How Can I Get My COE?

You can get your COE instantly through a VA Home Loan Specialist at Six Pillar Lending. We have access to the Veteran’s Administration’s system. If you are not in the VA’s system, we can still help you obtain your document. Ask us to get you the proper forms to fill out and expedite the process.

10. Eligibility is One Part of the VA Home Loan Process

Qualifying for a VA home loan is the most important part of the home-buying process for those who are eligible. The Veteran’s Administration only guarantees part of the loan… VA Lenders are the ones who give qualified Veterans and Servicemembers home loans.

Having a minimum credit score of around 580 combined with a debt-to-income (DTI) ratio lower than 50% usually meets lender requirements – residual income, however, can sometimes be considered as well. Knowing your financial situation and having paper documentation available to prove it is key when getting ready to purchase a property through VA loans!

Time to Get Your COE and Get Pre-Approved!

Contact the VA Home Loan Experts at Six Pillar Lending to obtain your Certificate of Eligibility and start your pre-approval process. All you need is your past two paystubs, the last two years of tax returns, and the last two months of bank statements to get started. Online submission of all of your loan documents is very easy and secure. If you have more questions about VA Home Loan benefits, Six Pillar Lending is here to help. Many of us are Veterans and come from military families, so we know first-hand your life experiences as well as the experience of getting a VA Home Loan from the borrower’s perspective. Get in touch with us today to get started.

Related Posts