Becoming Part of the Community Buying a home isn’t just about moving into a new…

Historical Mortgage Interest Rates

Mortgage interest rates are a key factor in the housing market, affecting both buyers and sellers. For many years, interest rates on mortgages have been an important indicator of the overall state of the economy. In this article, we will look at where mortgage interest rates are today and compare them to historical rates.

What is a Mortgage Interest Rate?

First, let’s define what we mean by “mortgage interest rate.” A mortgage interest rate is the rate at which a borrower pays interest on the money they borrow to purchase a home. This rate is usually expressed as a percentage and can vary depending on several factors, including the borrower’s credit score, the loan’s size, and the loan term’s length.

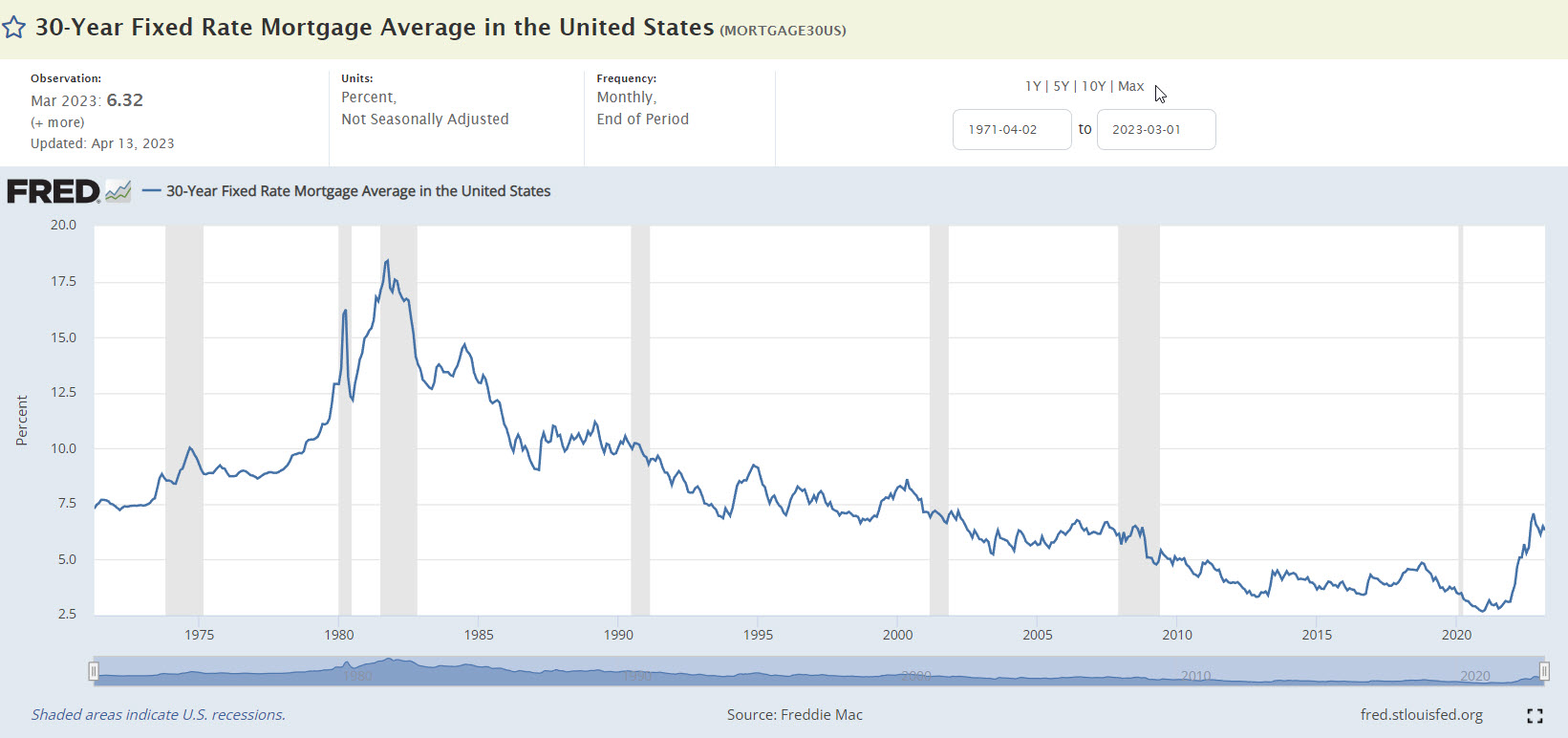

Historical Mortgage Interest Rates

To put current rates into perspective, it’s helpful to look at historical mortgage interest rates. The Federal Reserve has been tracking mortgage rates since 1971, and their data shows that rates have fluctuated significantly over the years. In the 1970s, mortgage rates were often above 10%, reaching a peak of 18.45% in October 1981.

In the 1990s, rates fell significantly, with the average 30-year fixed-rate mortgage falling below 7% by the end of the decade. Rates remained relatively stable in the early 2000s, hovering around 6%, until the housing market crash in 2008.

After the crash, the Federal Reserve lowered interest rates to stimulate the economy, and mortgage rates dropped to historic lows. The COVID pandemic brought on even lower rates, ultimately bottoming out in January 2021 at 2.65%.

Why Did Interest Rates Go Up?

When the economy is growing rapidly, demand for goods and services increases, which can lead to inflation. In order to prevent inflation from spiraling out of control, the FED may raise interest rates to reduce borrowing and spending, which can slow down economic growth.

Additionally, the FED may raise interest rates if they believe that the economy is overheating, which can lead to a bubble in asset prices. By raising interest rates, the FED can make it more expensive for investors to borrow money to invest, which can help to prevent a bubble from forming.

The FED began raising interest rates back to normal in January 2022, and today’s 30-Year Fixed Rate Mortgage interest rate is at 6.39%. So when looking at rates in a historical context, today’s rates are still low compared to historical averages, but they have increased slightly from the all-time lows of about a year ago.

Bottom Line

In conclusion, mortgage interest rates are currently low compared to historical rates, making homeownership more accessible for many people. While low-interest rates can stimulate economic growth, they can also contribute to an overheated housing market and asset bubbles. As always, it’s important to stay informed and make decisions based on your individual financial situation and the current state of the market.

Related Posts